We show you the money. Payments. Growth.

Paybyrd, Europe's premier Personalized Payment Platform. Our focus is on simplicity and efficiency when it comes to payments.

Paybyrd empowers businesses with unrestricted enterprise capabilities by integrating omni-channel payment methods into a tailored payment encounter.

Solutions tailor-made for your business model

We recognize that every business has unique needs. Our goal is not to dictate how you should process payments, but rather to enable you to create a payment experience that aligns with your vision.

Subscriptions

E-commerce

In-store payment

QR Code Payments

Social Payments

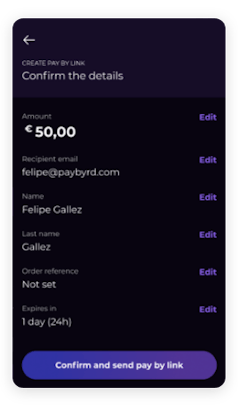

Pay by Link

In-store Cashless

Mass Transit

Connect a single platform to all kinds of payments. In-person, e-commerce, business payments, social payments.

With an average payment acceptance rate above 92.7%, sell more, earn more. Supercharge your growth.

With full control over all tokens, build new business models, create enriching loyalty experiences. Dazzle your customers.

Once integrated, don’t ever look back. Get Updates, activate new features, new possibilities, without changing a single line of code.

Ambition is the lifeblood of any enterprise with aspirations for growth. At Paybyrd, we are committed to empowering you to unleash that potential for expansion, no matter the scale of your ambitions. Let us help you achieve your goals and drive your business forward.

Including:

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get started with Paybyrd.

Get onboarded in minutes. Start accepting live payments in a matter of hours.